We’re excited to introduce support for short and leveraged exposure in Model Portfolios. You’re no longer limited to long-only portfolios – and can now construct models with short and leveraged positions and adjust allocations dynamically over time.

Note: Long/Short & Leveraged models are available only in the Advisor Pro plan.

Getting Started

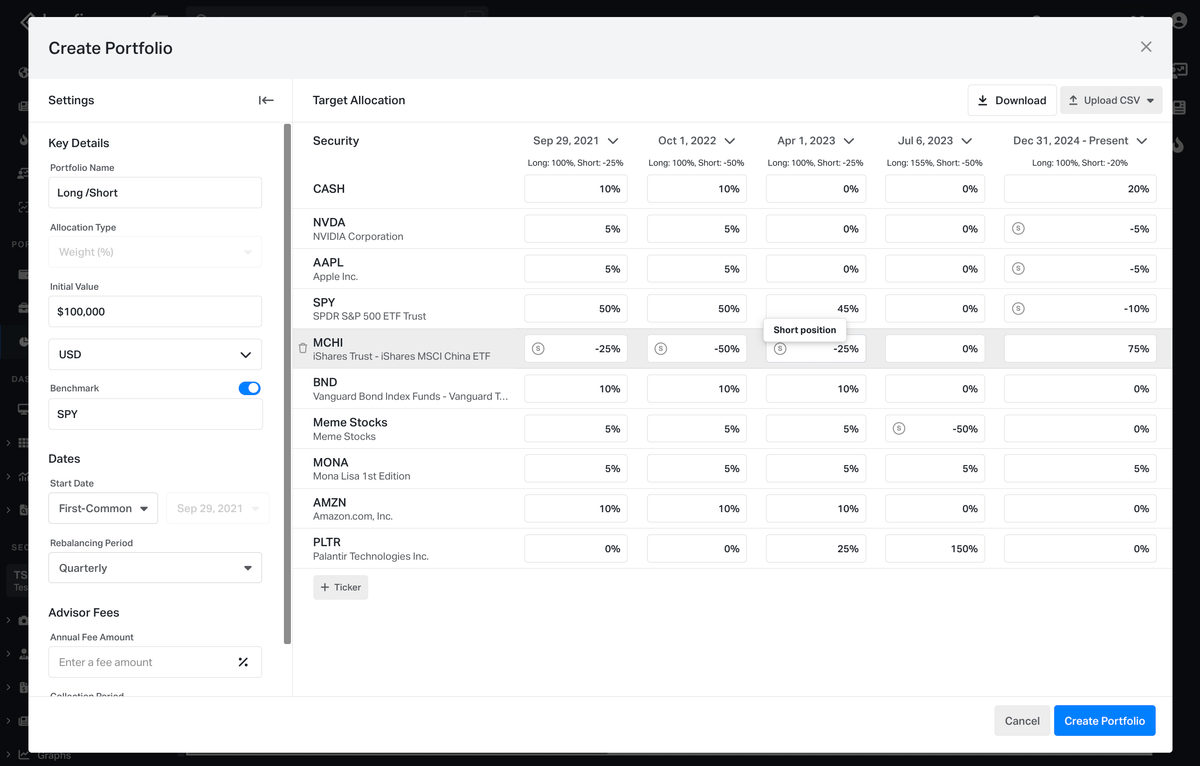

You can create model portfolios with short and leveraged exposures manually (using the ‘from scratch’ option) and by CSV. The portfolio editor is no longer restricted to weights of between 0% and 100% for the individual positions and the model.

To add short weights, place a ‘-’ sign before the weight, after which an ‘S’ icon will appear to indicate the short. To add leveraged weights, you can add weights above 100% for individual positions or a collective exposure of greater than 100% for the model.

Key Changes

Portfolio Editor

- Negative Weights: Enter negative values for short positions.

- Short Position Indicator: An ‘S’ icon appears next to short positions.

- Values Above 100%: Enter values exceeding 100% to create leveraged positions, and

- CSV Import: Now supports negative weights for shorts and values above 100% for leverage. You can now have individual positions that exceed 100%, as well as net portfolio exposure that exceeds 100%.

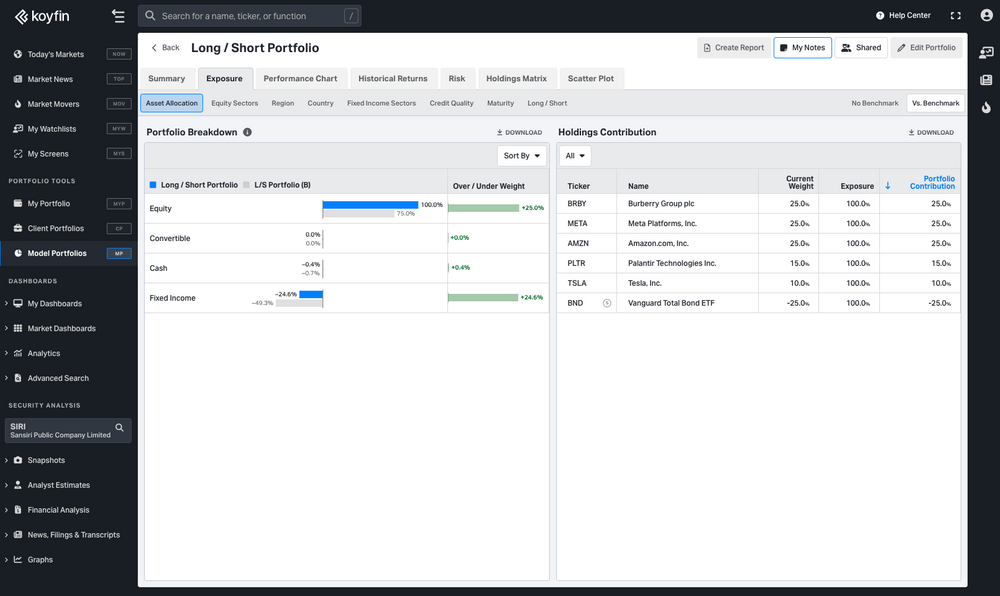

- Allocation Display: Shows the allocation split between "Long" and "Short" when you create a long / short portfolio.

Exposure

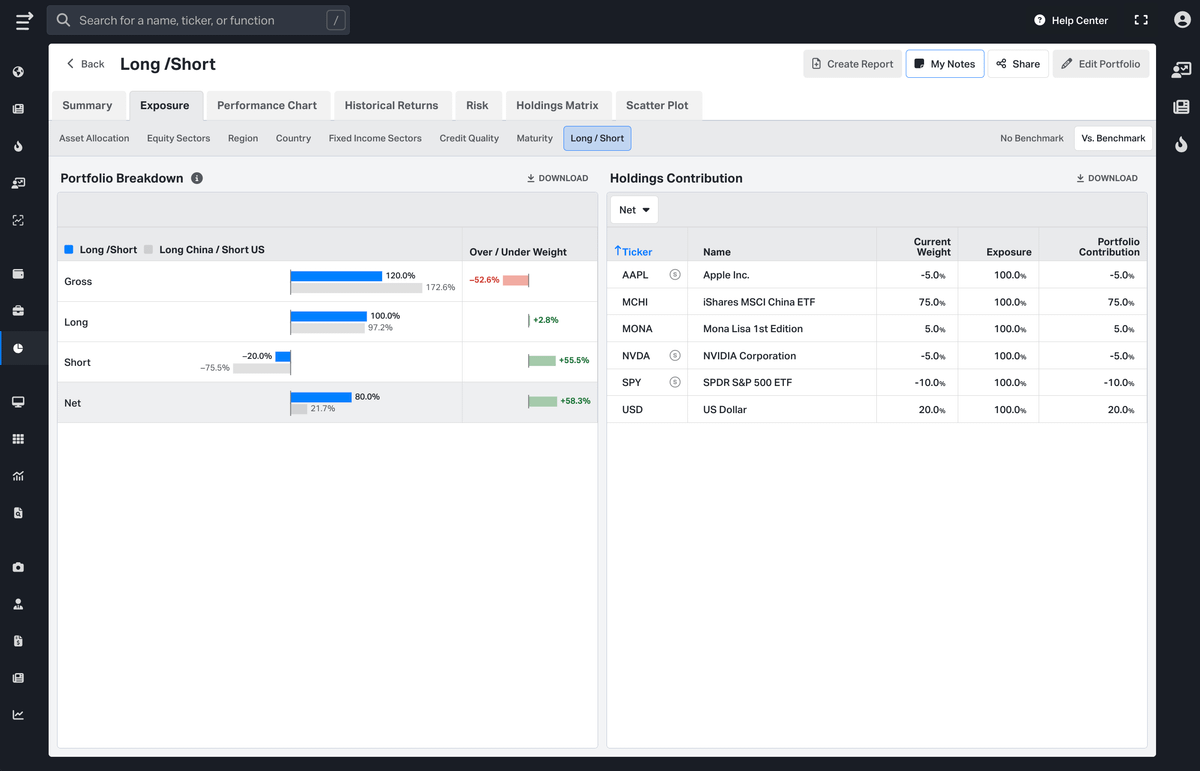

For portfolios containing short and/or leveraged positions, exposures are presented using bar charts only.

For the Asset Allocation, Holdings, and Region (All) and Country (All) exposures, the data will be presented as a net value relative to the gross portfolio exposure.

For example, this Long (100%) / Short (25%) portfolio is 100% long equity and 25% short fixed income. If the portfolio added a further 25% short in Nvidia (NVDA, Equity) the portfolio would be 100% long and 50% short and display 75% net equity exposure and -25% net fixed income exposure.

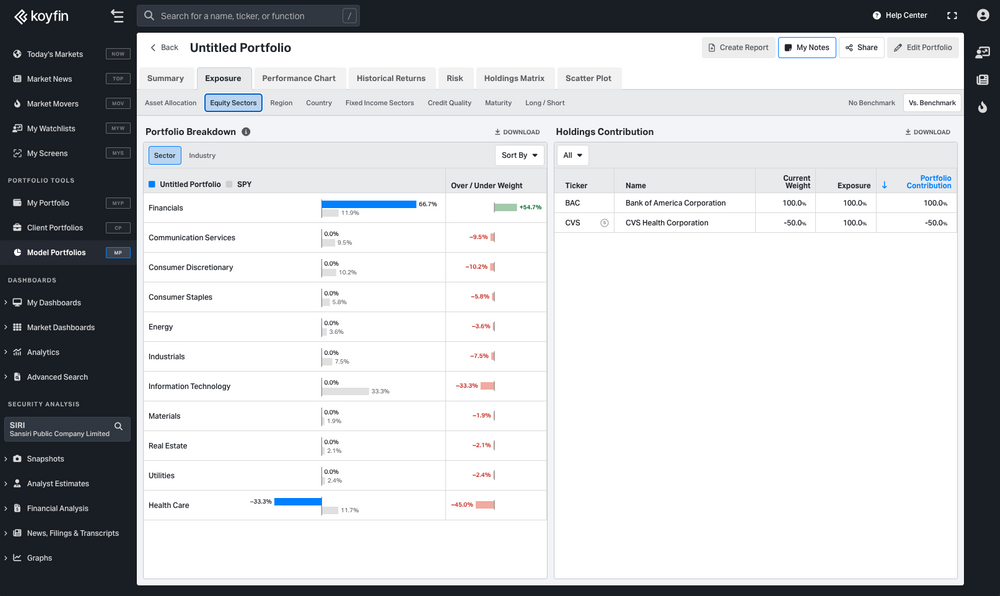

In all other exposure exhibits, the data will be presented as a net value relative to the gross value of the subcategory (namely, equity or fixed income).

For example, if a portfolio was 100% long the Financials Sector and 50% short the Healthcare sector, the gross exposure is 150%.

Financial exposure would be presented as 100% / 150% = 67%.

Healthcare exposure would be presented as -50% / 150% = -33%.

New "Long/Short" Exhibit

A dedicated visualization for portfolios with leverage or shorts that breaks down the gross, long, short, and net exposure.

- Sorting Options: A new dropdown menu allows you to toggle between sorting by:

- Gross exposure (total of all positions)

- Long exposure (sum of positive positions)

- Short exposure (sum of negative positions)

- Net exposure (longs minus shorts)

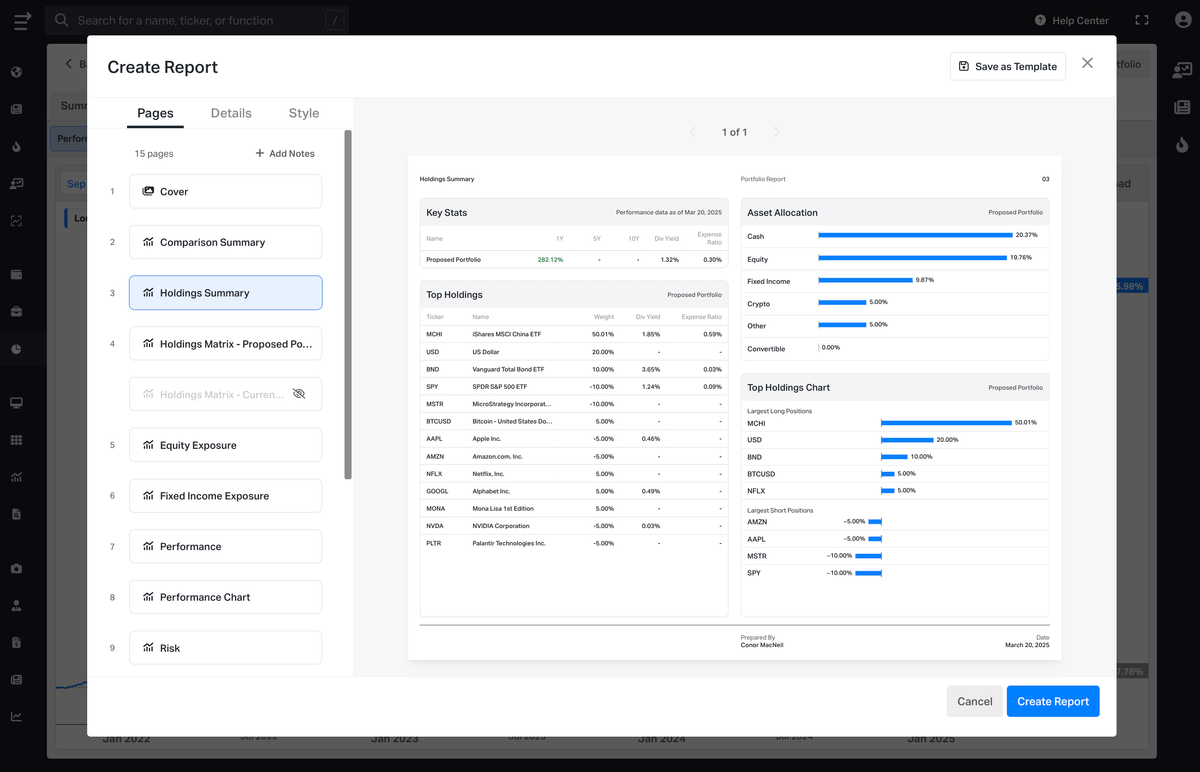

Reports Enhancements

Short and leverage exposures are now supported in reports and dynamically adjust depending on the make-up of your portfolio.

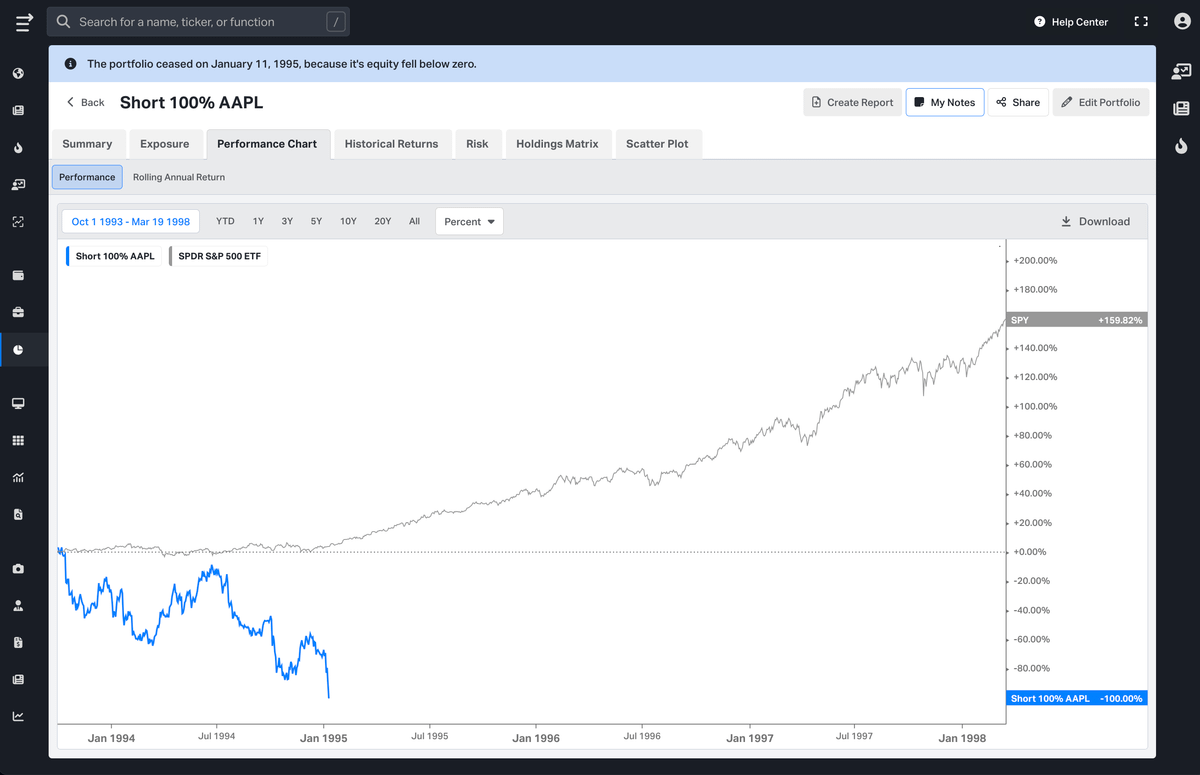

Bankrupt Models

With the introduction of shorts and leverage, we have introduced the potential for a model’s equity value to fall below zero.

Should this happen, the performance and holdings data will terminate on the date the portfolio’s equity value falls below zero. A banner will appear at the top of the model, indicating this has happened, and the date of termination.

For more context on model portfolio construction, see this help article.